Section 1

Financial Behaviour

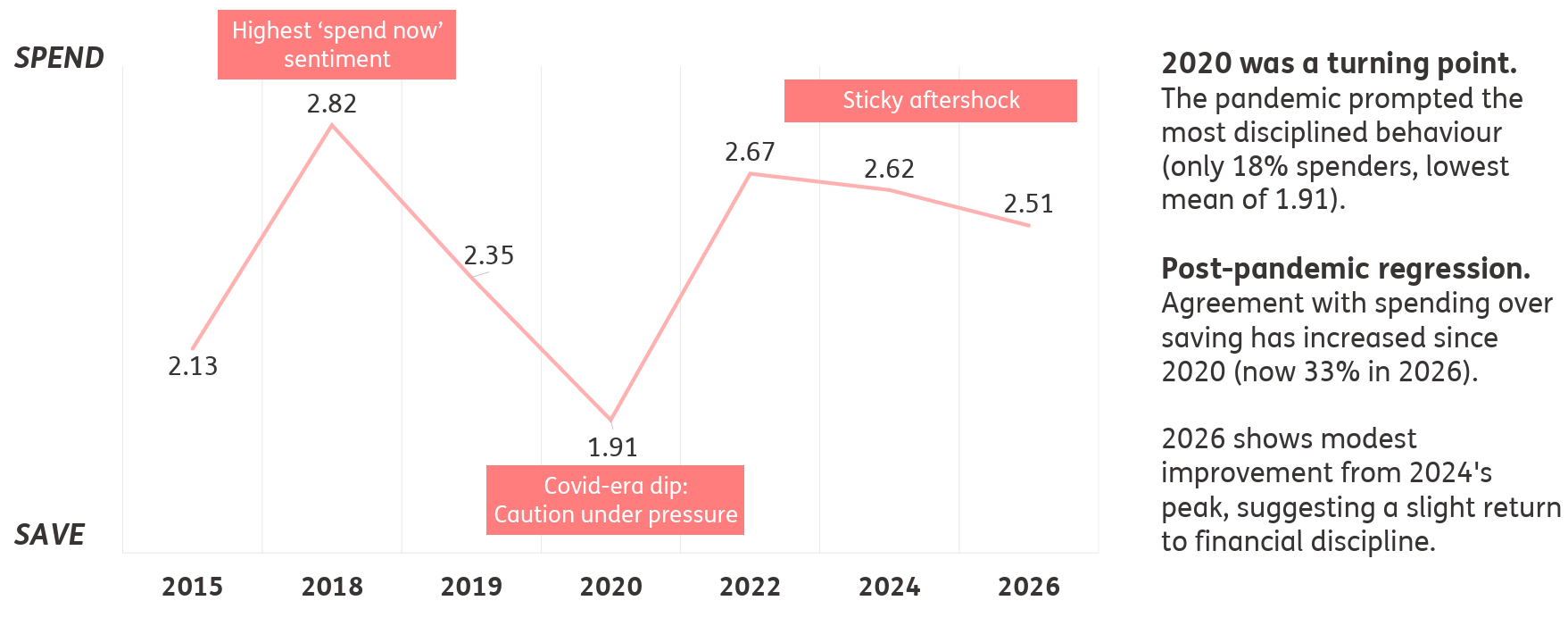

Pressure-driven changes

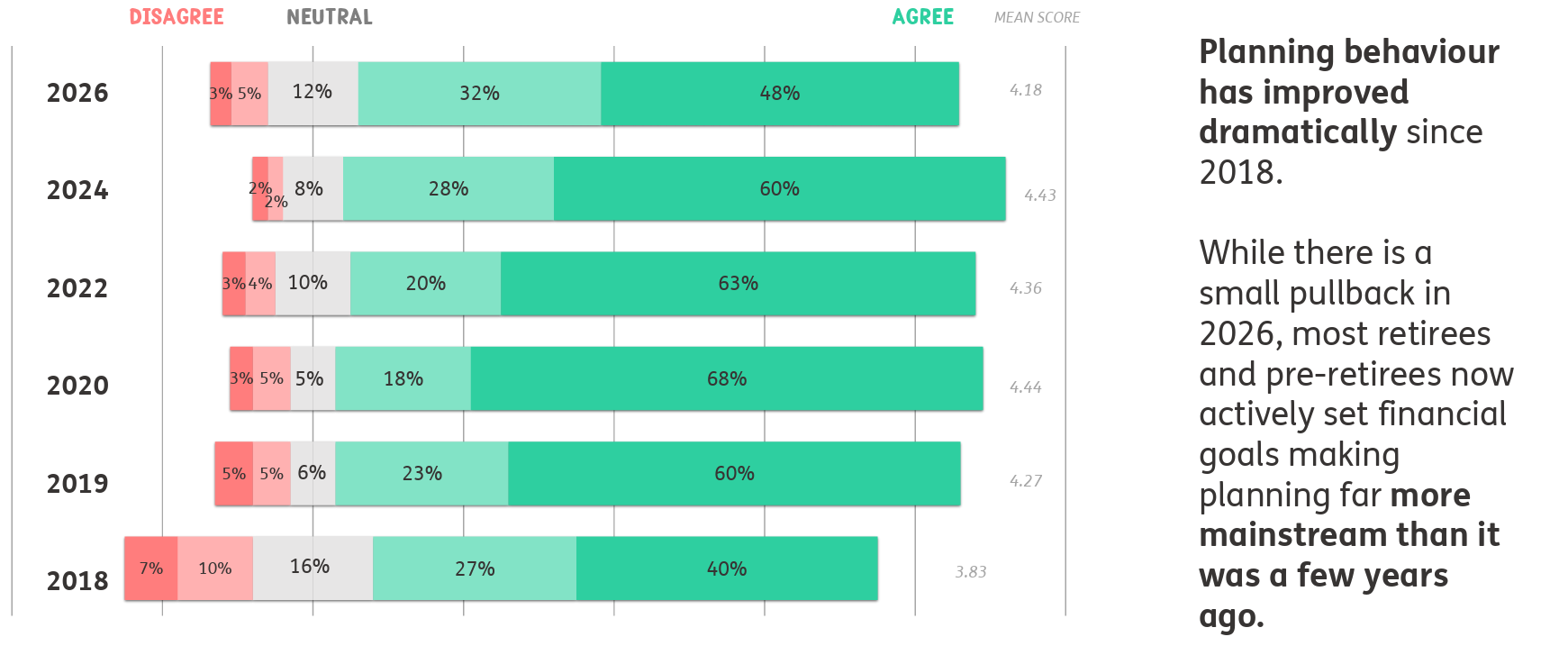

Establishing clear retirement goals

Mean score (1=Strongly disagree, 5=Strongly agree) for: I plan my finances. I set goals that I want to achieve and work towards that.

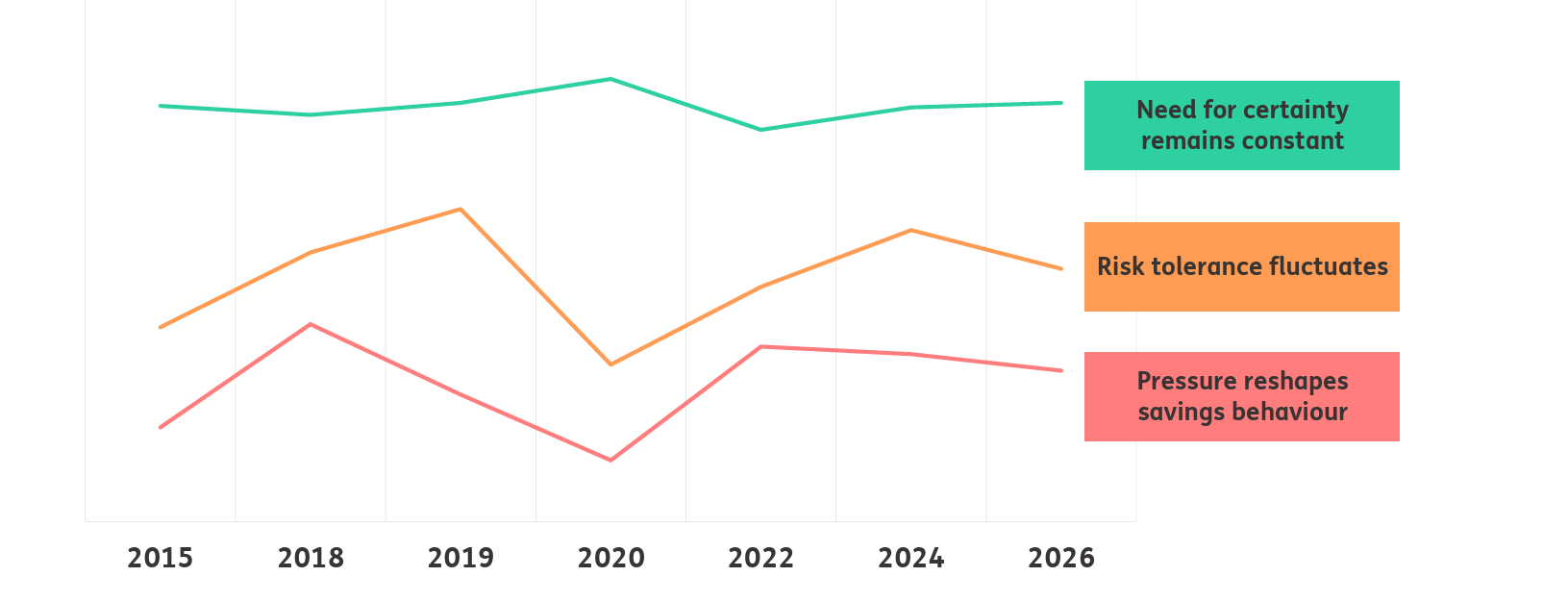

Caution rose under pressure, and it has stuck

Mean score (1=Strongly disagree, 5=Strongly agree) for: “I do not save much or plan for the future; I prefer to spend money when I have it.”

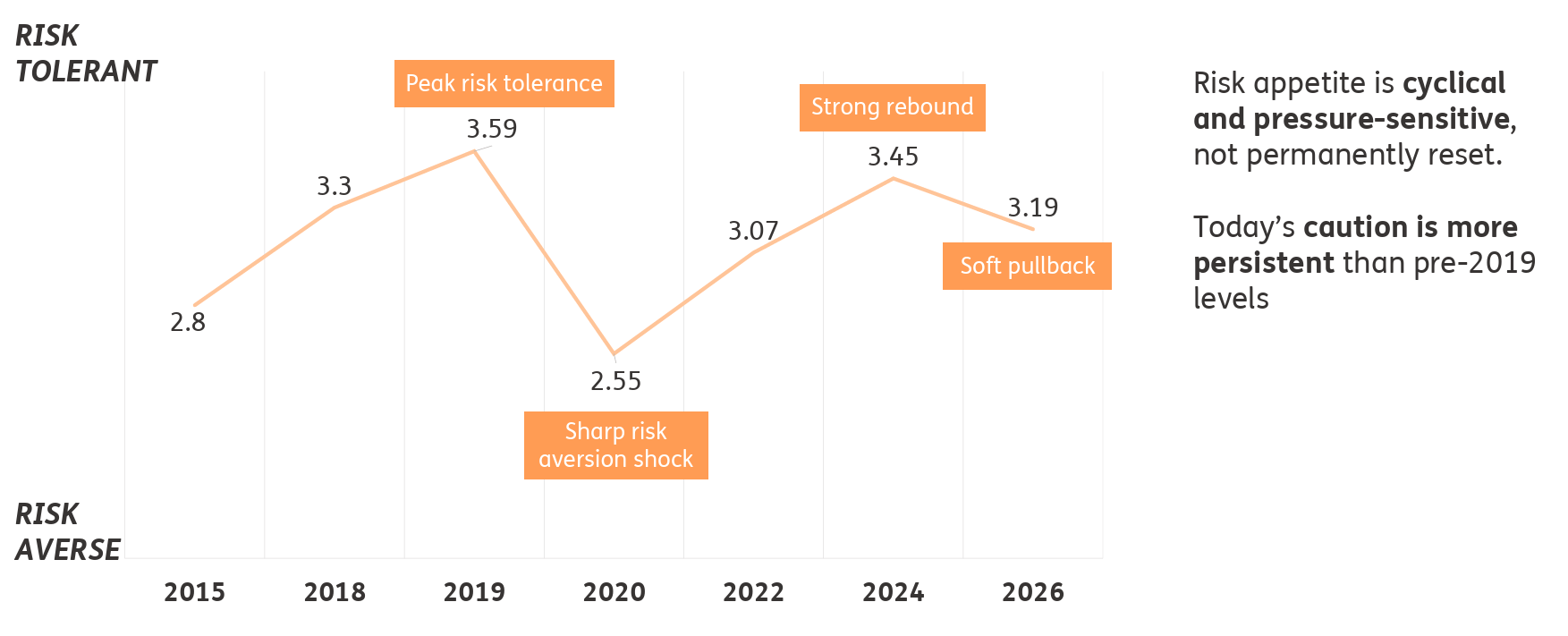

Risk appetite falls under pressure and only partially recovers

Mean score (1=Strongly disagree, 5=Strongly agree) for: “I do not mind taking risks with my money for saving or investment purposes.”

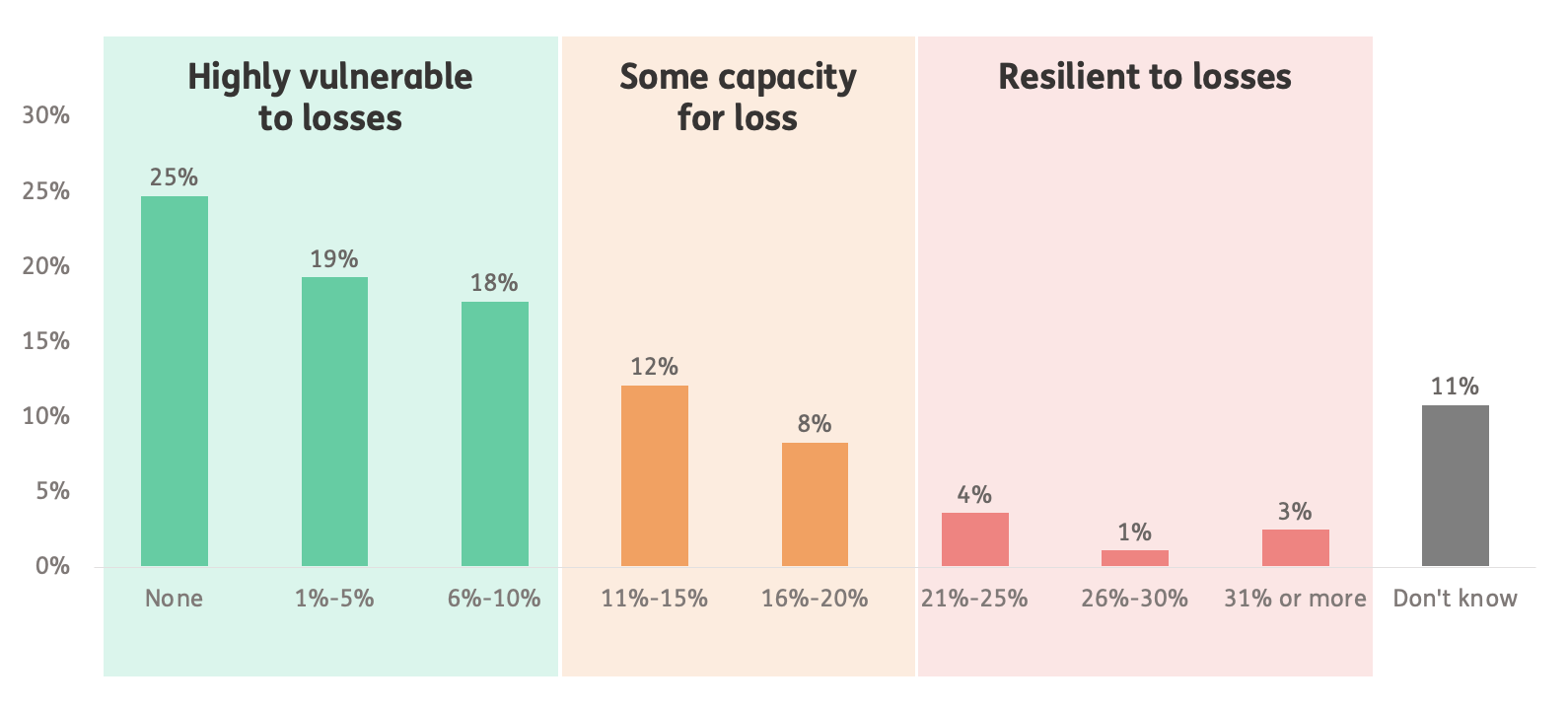

Only 8% of retirees claim to be resistant to market shocks

What percentage do you think you could afford to lose in a market crash before it seriously impacts your retirement plans?

INSIGHTS

Overall capacity to absorb losses remains very low

- People may be forced to spend less but they still hesitate to take risk with what they have.

- Savings behaviour: Caution becomes sticky.

- Risk behaviour: Confidence rebounds but incompletely.

- Confidence returns faster than caution, but risk appetite has not fully reset.

- While risk appetite fluctuates, capacity for loss is structurally low among pensioners.

- For the vast majority, even a moderate market fall would threaten their retirement security – reinforcing why certainty, not volatility, dominates retirement decision-making.

Under pressure, behaviour changes but preferences don’t

Preference for guaranteed monthly income that does not change with market conditions stays tightly between 77% and 86%

Mean score (1=Strongly disagree, 5=Strongly agree) for: “I prefer a secure, guaranteed monthly income in retirement over an income that might change depending on investment returns.”