Section 2

Retirement Confidence

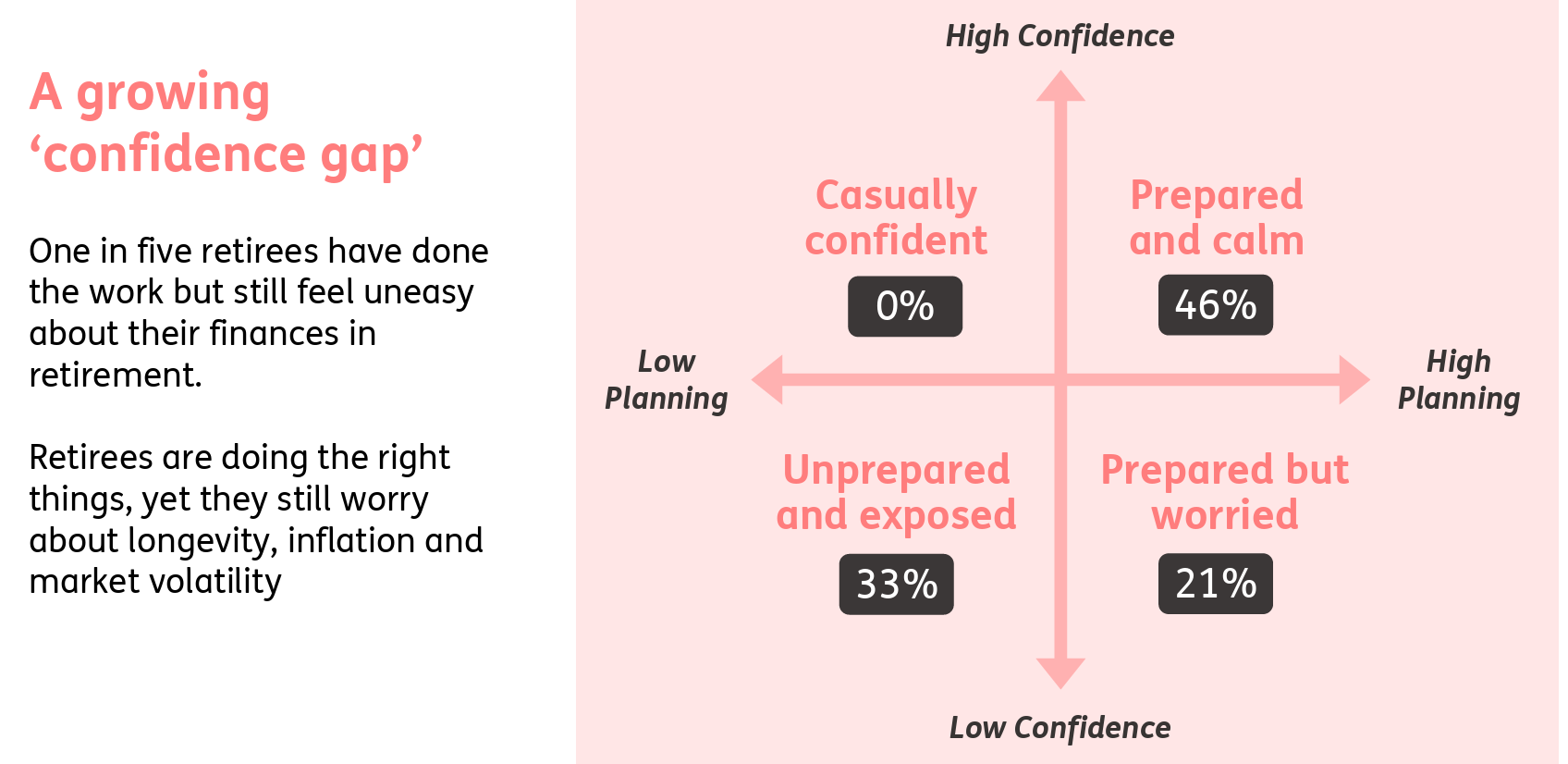

Ready or not?

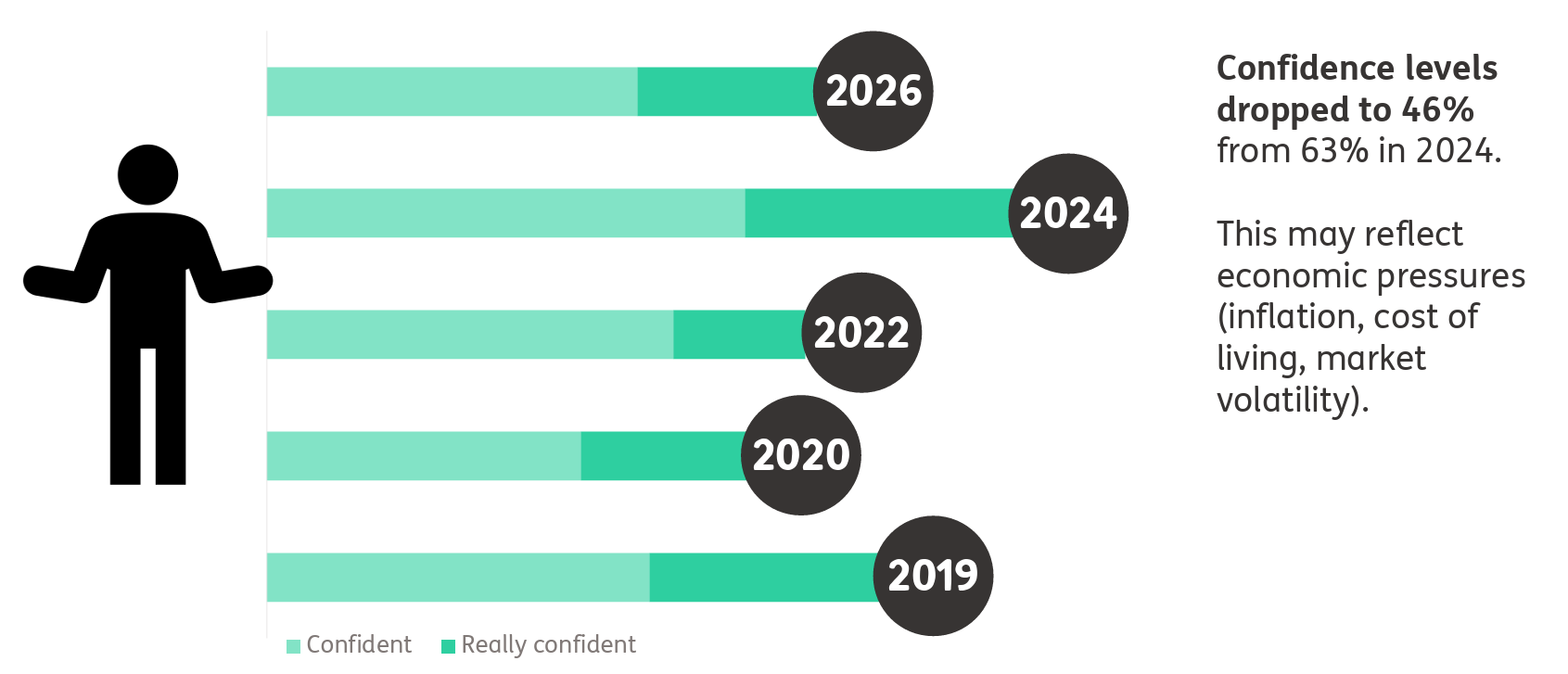

Financial confidence for retirement remains fragile

Mean score (1 = Really not confident, 5 = Really confident) for: "How confident are you that your money will cover your monthly expenses in retirement if you reach the age of 100, allowing for inflation?"

People are planning, but they don’t feel secure

INSIGHTS

Growing retirement anxiety

- The 2026 drop in confidence suggests people are increasingly worried about outliving their money.

- Rising cost of living may be driving pessimism.

- High uncertainty rates suggest many retirees lack clear visibility into their financial future.

- Planning is no longer the problem. The real shift we’re seeing is not a lack of effort, it’s a lack of certainty.

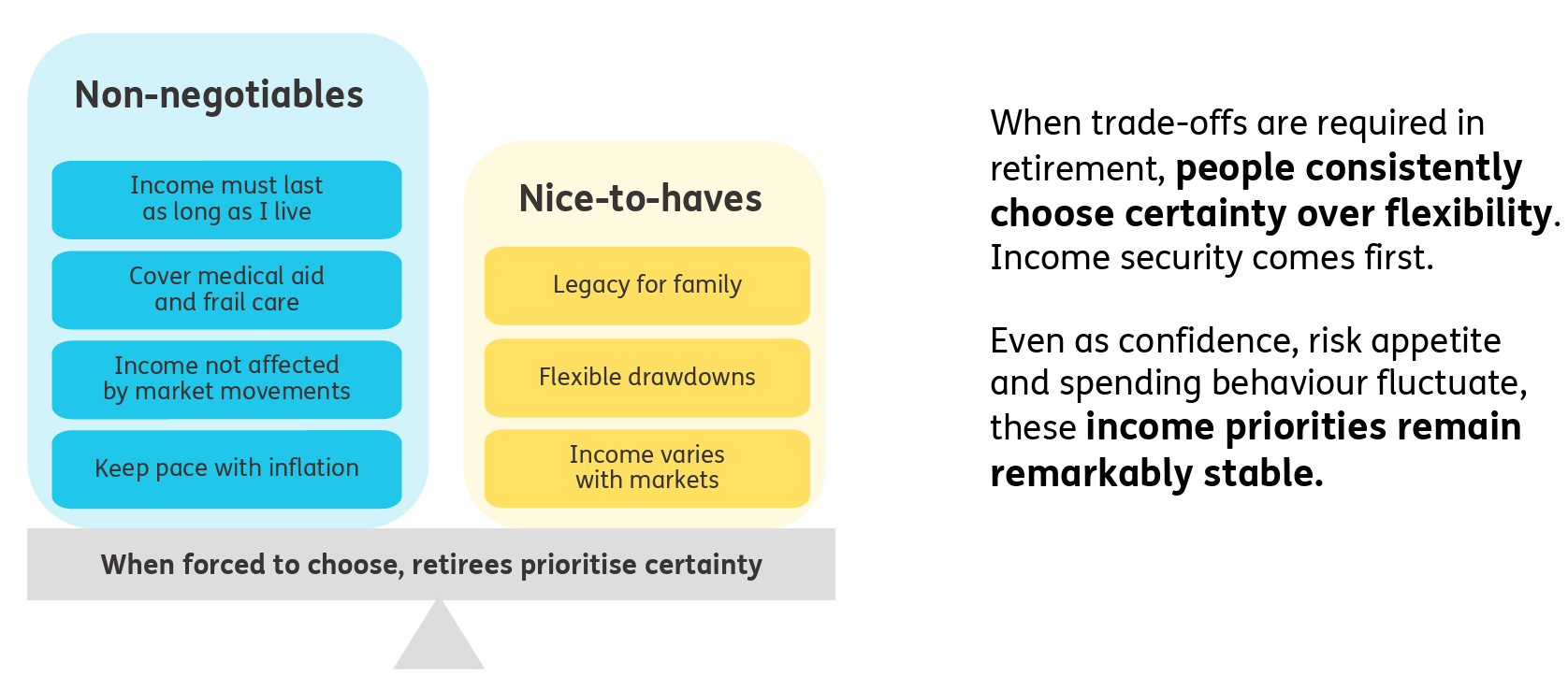

Certainty consistently outranks flexibility

Mean score (5 = Extremely important, 1 = Not important) for: Importance of how you will use your retirement savings when you retire

The shift isn’t in priorities – it’s in strain

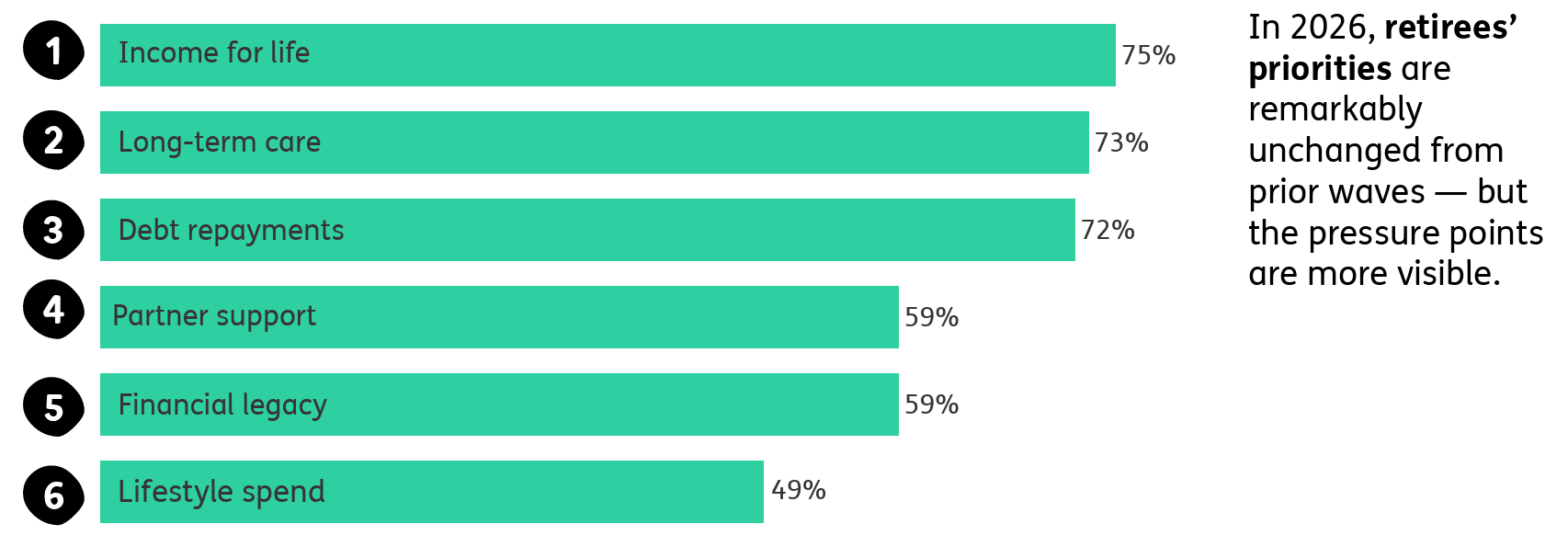

Importance of what retirement savings must cover

Mean score (5 = Extremely important, 1 = Not important) for: Importance of how you will use your retirement savings when you retire. Those expressing extremely and very important indicated above.

INSIGHTS

Retirement savings shift from lifestyle to survival

- In 2026, lifetime income is still non-negotiable.

- Generating an income for life remains the clear, dominant objective, still ranking highest across all years. This reinforces that longevity risk continues to outweigh all other considerations.

- Covering long-term care and medical needs stays very high, indicating growing awareness of later-life costs rather than discretionary goals.

- Rising pressure means retirement savings are increasingly being used to manage risk and debt, not just lifestyle.